While you join Betterment, you may set an funding purpose that you just wish to save in direction of. You may set numerous funding objectives. While you create a brand new funding purpose, ask for the anticipated period of the purpose and choose one of many following purpose varieties:

Main Purchases Training Retirement Retirement Revenue Basic Investments Emergency Fund

Betterment additionally permits customers to create money objectives by way of its Money Reserve providing and crypto objectives by way of its crypto ETF portfolio. These purpose varieties are outdoors the scope of this allocation recommendation methodology.

For all funding objectives (excluding emergency funds), Betterment shall be knowledgeable of your plans to make use of your funds and withdraw your funds (i.e. full speedy liquidation within the case of a significant buy or partial periodic liquidation within the case of retirement), relying on the anticipated time interval and the kind of purpose chosen. An emergency fund, by definition, has no anticipated time interval (when setting objectives, Betterment assumes an emergency fund time interval to tell financial savings and deposit recommendation, however this may be edited and doesn’t have an effect on the beneficial funding allocation). It’s because you can’t predict when an surprising expense will happen or how a lot it should price.

For all objectives (besides emergency funds), Betterment recommends funding allocations based mostly on the time interval and purpose kind you select. Betterment creates beneficial funding allocations by predicting varied market outcomes and averaging one of the best performing threat ranges throughout the fifth to fiftieth percentiles. For emergency funds, Betterment’s beneficial funding allocation gives the potential for progress whereas limiting the danger of drawdowns of not more than a beneficial buffer above the quantity wanted in an emergency.

Beneath are beneficial funding allocation ranges by purpose kind, excluding emergency funds.

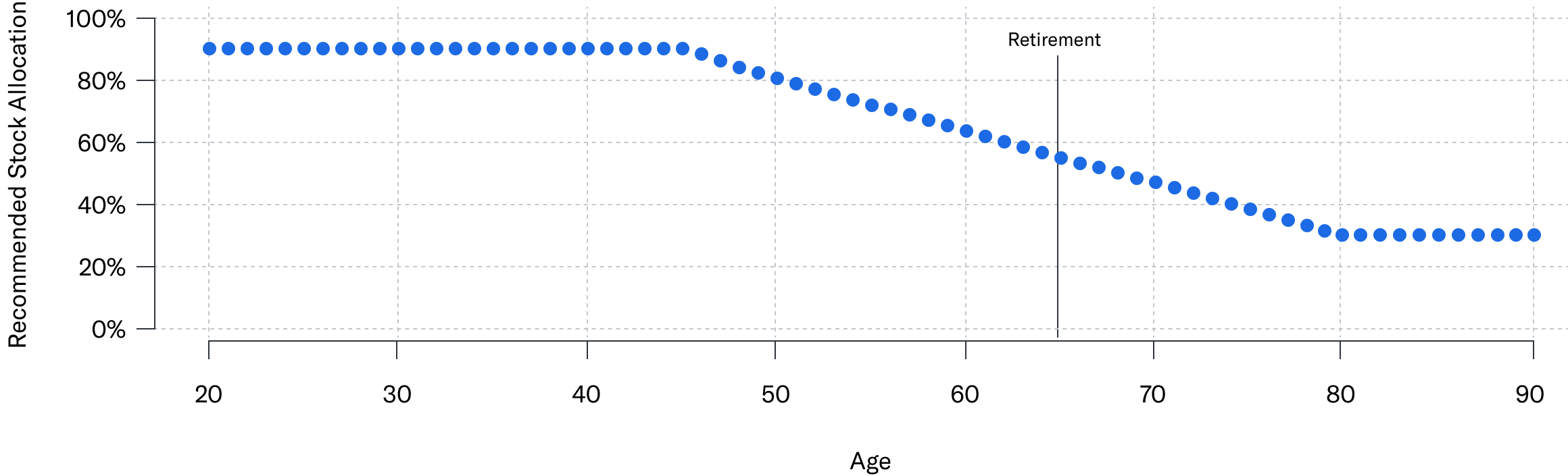

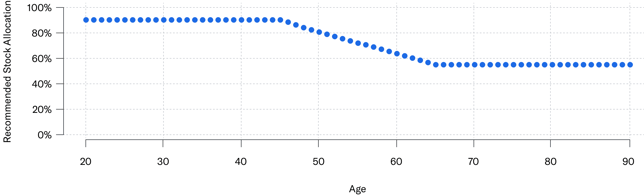

Aim Sort Most Aggressive Allocation Suggestion Most Conservative Allocation Suggestion Massive Buy 90% Shares (33+ years) 0% Shares (at maturity) Training 90% Shares (33+ years) 0% Shares (at maturity) Retirement 90% Shares (20+ years till retirement) 56% Shares (at retirement age) Retirement Revenue 56% Shares (24+ years life expectancy) 30% Shares (9 Basic Investments 90% Shares (20 years or extra) 56% Shares (if the interval is reached)

As you may see from the desk above, usually talking, the longer the time horizon of your purpose, the extra aggressive the allocation beneficial by Betterment. And the shorter the time horizon of your purpose, the extra conservative the allocation that Betterment recommends. This creates what is called a “glide path” through which beneficial allocations for particular purpose varieties are adjusted over time.

Beneath is the whole glide path that applies to the purpose varieties offered by Betterment.

Fundamental buying/instructional objectives

Retirement allowance/retirement revenue goal

The diagram above reveals a hypothetical instance of a shopper who lives to be 90 years outdated. It doesn’t characterize precise shopper efficiency and isn’t indicative of future outcomes. Precise outcomes could fluctuate relying on a wide range of elements, together with buyer modifications within the account and market fluctuations.

The diagram above reveals a hypothetical instance of a shopper who lives to be 90 years outdated. It doesn’t characterize precise shopper efficiency and isn’t indicative of future outcomes. Precise outcomes could fluctuate relying on a wide range of elements, together with buyer modifications within the account and market fluctuations.

Basic funding objectives

Betterment provides an “auto-adjust” function that routinely adjusts your purpose’s allocation to regulate the danger of the relevant purpose kind, turning into extra conservative as you method the tip of your purpose’s funding schedule. Step by step change the danger degree and create a easy glide path.

As a result of Betterment adjusts glide path beneficial allocations and portfolio weights based mostly in your particular objectives and time horizon, you will discover that your “Main Purchase” objectives take a extra conservative path in comparison with a retirement or basic investing glide path. Within the very quick time period, the danger is nearly zero, as you’re anticipated to totally liquidate your funding by the scheduled date. With a retirement purpose, you anticipate to obtain distributions over an extended time frame, so it could be a good suggestion to keep up a better threat allocation even after the goal date is reached.

Auto-adjustment is accessible for funding objectives which have an related time interval (emergency fund objectives, goal revenue constructed with BlackRock portfolios, and Goldman Sachs Tax Good Bond Portfolio) Betterment Core Portfolio, SRI Portfolio, Innovation Expertise Portfolio, Worth Tilt Portfolio, and Goldman Sachs Good Beta Portfolio. In order for you Betterment to routinely modify your investments based on these glide paths, you have got the choice to allow Betterment’s auto-adjust function if you settle for Betterment’s beneficial allocations. This function helps you match your goal allocations with beneficial allocations utilizing reactive and proactive rebalancing.

Regulate threat tolerance

The funding allocation suggestions and glide path described above are based mostly on so-called “threat capability,” or the extent to which a shopper’s goals can stand up to monetary setbacks based mostly on the anticipated time horizon and liquidation technique. The shopper has the choice to just accept or deviate from this advice.

Betterment makes use of an interactive slider that enables shoppers to change between totally different funding allocations (how a lot to allocate to shares and bonds) till they discover an allocation that takes their threat tolerance into consideration and meets the anticipated vary of progress outcomes they will expertise for his or her objectives. Betterment’s slider contains 5 classes of threat tolerance.

Very Conservative: This threat setting is related to an allocation that’s greater than 7 proportion factors under our beneficial allocation to equities. So long as you’re conscious that you could be be sacrificing potential income as a way to restrict the potential for losses occurring, you’re fantastic. It’s possible you’ll want to avoid wasting extra to succeed in your purpose. This setting is appropriate for individuals with low threat tolerance. Conservative: This threat setting is related to an allocation that’s 4 to 7 proportion factors under our beneficial allocation to equities. So long as you’re conscious that you could be be sacrificing potential income as a way to restrict the potential for losses occurring, you’re fantastic. It’s possible you’ll want to avoid wasting extra to succeed in your purpose. This setting is appropriate for individuals with low threat tolerance. Reasonable: This threat setting is related to an allocation inside 3 proportion factors of the beneficial allocation to equities. Aggressive: This threat setting is related to an allocation that’s 4 to 7 proportion factors above our beneficial allocation to shares. This will lead to larger income in the long run, however could expose you to higher losses within the quick time period. This setting is appropriate for individuals with a excessive tolerance for threat. very aggressive: This threat setting is related to an allocation that’s greater than 7 proportion factors above our beneficial allocation to equities. This will lead to larger income in the long run, however could expose you to higher losses within the quick time period. This setting is appropriate for individuals with a excessive tolerance for threat.